Payment Infrastructure for Digital Platforms

Many businesses refer to payment infrastructure when integrating payment processes. In practice, however, this often means relying on external systems without direct control over processing, routing, or banking relationships.

This distinction becomes critical for digital platforms.

Platform-based models such as digital content services, creator economy setups, or subscription businesses process large volumes of transactions with varying requirements in risk management, settlement, and international payment flows. Simple payment integration is not sufficient in these cases.

A true payment infrastructure provides the operational foundation to actively manage transactions, orchestrate payment flows, and handle complex settlement logic. This includes direct acquiring connections, dedicated merchant accounts, and a controlled processing structure.

Unlike traditional e-commerce setups with linear payment flows, platforms must manage multi-layered transaction structures. Revenues are distributed across multiple parties while supporting international users, currencies, and regulatory requirements.

A high-performance infrastructure consolidates these processes within a controlled system environment. Through a dedicated processing layer, transactions are not only routed but actively managed and optimized.

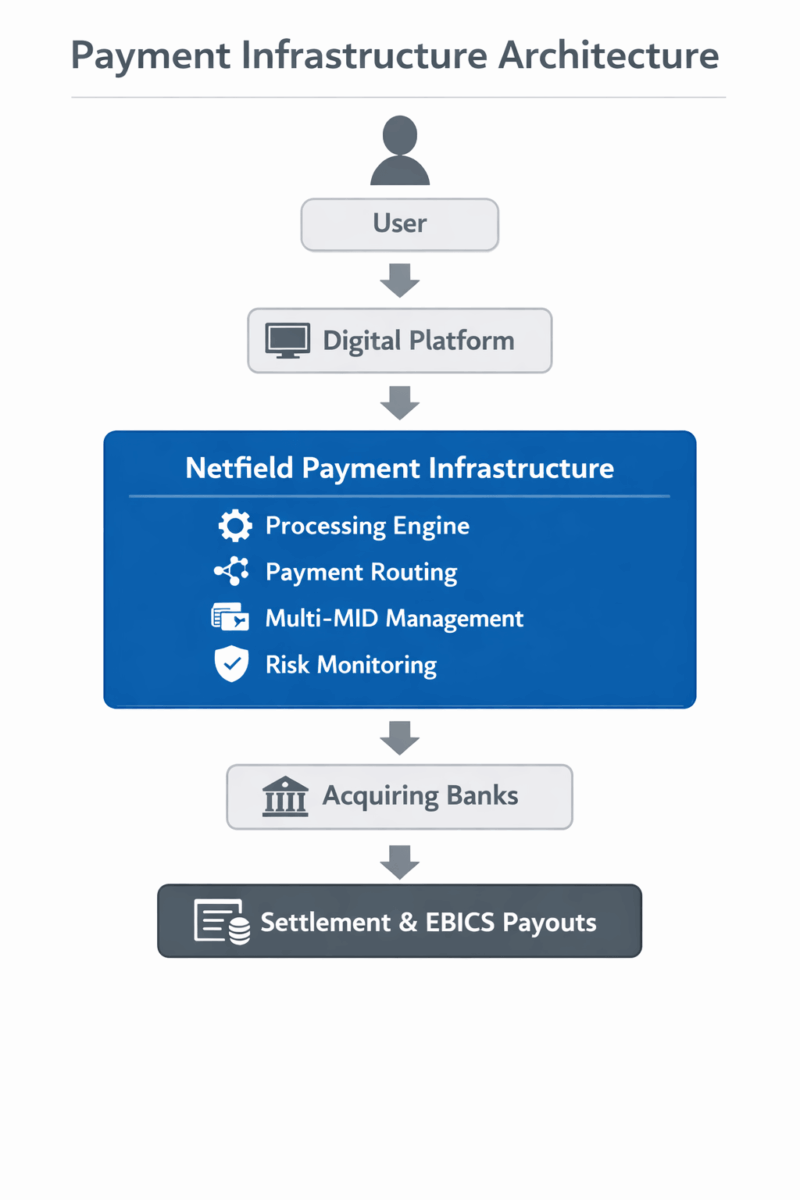

In this context, Netfield Media operates a dedicated high-end processing layer where merchant accounts, acquiring connections, and routing logic are integrated within a controlled system environment. This enables payment processes to be actively managed and continuously optimized rather than simply integrated.

This architecture provides the control required to operate stable and scalable payment systems. The differences compared to standardized models become particularly clear in the context of aggregator vs payment infrastructure.

What truly defines a payment infrastructure

The term payment infrastructure is widely used, yet in practice it often refers to very different types of systems. Many solutions labeled as infrastructure merely forward payment requests without providing actual control over the underlying processes.

A true payment infrastructure goes far beyond that.

It is not only about processing transactions, but about the ability to actively manage, analyze, and operate payment flows. This includes direct acquiring connections, dedicated merchant accounts, and the ability to dynamically route transactions based on specific requirements.

The key difference lies not in functionality, but in control. While basic payment solutions simply forward transactions, an independent infrastructure enables active control over processing, risk, and settlement within a proprietary system environment. How this controlled path actually runs from checkout to the issuer decision is outlined in from checkout to issuer.

How these structural differences manifest in practice and why many payment setups become unstable despite working integrations is explained in detail in the following article. → Understanding Adult Payment Problems

This distinction becomes particularly relevant in complex digital business models. Platforms, subscription services, and international payment environments require more than technical integration—they require a structure capable of operating payment processes in a stable, flexible, and scalable way. “How these structural differences play out in practice and why many payment setups become unstable despite working integration is also shown in our article on why adult payment is now an infrastructure question.

Payment infrastructure for platform models

Digital platforms differ fundamentally from traditional e-commerce. While online shops focus on selling individual products, platform-based models monetize content, interactions, or services within a broader digital ecosystem.

Typical examples include creator platforms, community or social networks, dating services, as well as streaming and content platforms. These models often combine multiple monetization strategies, such as credits, subscriptions, and direct user-to-user payments.

As a result, payment structures become significantly more complex than in standard e-commerce. It is no longer just about accepting payments, but about processing, distributing, and reconciling revenues across multiple participants.

A robust payment infrastructure provides the operational foundation to manage these processes in a controlled way. It enables payment flows to be actively managed, allocated, and structured across different stakeholders, while supporting international users, currencies, and regulatory requirements.

In practice, this means payment processes evolve from linear transactions into dynamic systems. Revenues must be distributed between platforms, creators, or partners, while maintaining stability, transparency, and scalability.

Many of these models operate within high risk payment environments, as they combine international transactions, digital content, and recurring billing. A more detailed explanation of these structures can be found here: High Risk Payment

Platforms dealing with digital content, particularly in creator economy, dating, or adult segments, often require specialized payment setups. In the context of adult payment processing, additional requirements arise regarding risk assessment, banking relationships, and compliance. Adult Payment for platforms

In these environments, simple payment integration is not sufficient. What matters is an infrastructure capable of operating payment processes in a stable and controlled manner over time. For creators and platforms looking for an operational solution for exactly this, Netfield Media offers a payment infrastructure for creators and platforms.

Payment routing and multi-MID architecture

A key component of modern payment infrastructure is the ability to control transactions through intelligent routing. Instead of being processed statically, payment requests are dynamically directed to different merchant accounts or acquiring banks based on defined parameters.

At its core, this is about more than processing payments—it is about actively optimizing payment flows.

A multi-MID architecture allows transactions to be distributed flexibly depending on factors such as origin, card type, geographic region, or risk profile. This creates a system that adapts to varying requirements rather than relying on a single processing structure.

In practice, this results in significantly higher stability. Failures in individual connections can be compensated, while approval rates can be improved through optimized routing decisions. Routing therefore becomes an operational control mechanism rather than just a technical feature.

Netfield Media operates an infrastructure where multiple merchant accounts and acquiring connections are integrated within a controlled processing layer. This enables transactions to be analyzed, evaluated, and routed in real time to the most suitable processing path.

In international or high-risk payment environments, this level of control is essential. It ensures stable payment operations while allowing flexible adaptation to changes in banking requirements, user behavior, or risk conditions.

Payment infrastructure and merchant of record

Beyond technical architecture, the underlying operating model plays a critical role in payment processing. In many cases, payment infrastructure is complemented by a merchant of record model, which takes on additional operational and regulatory responsibilities.

Within this setup, the merchant of record acts as the official merchant toward banks and payment networks. This allows platform operators to utilize payment processes without having to fully manage regulatory requirements, banking relationships, or compliance structures themselves.

The scope of responsibility goes beyond payment processing itself and includes merchant account management, risk control, chargeback handling, and settlement operations. These elements are integral to the overall payment architecture.

In this context, Netfield Media combines its own payment infrastructure with a merchant of record model, creating an environment where technical processing, regulatory responsibility, and operational control are unified.

This combination enables platform operators to leverage an existing infrastructure while maintaining stability, compliance, and scalability. A detailed explanation of this model can be found here: Merchant of Record

Especially in international or complex payment environments, the interaction between infrastructure and operating model becomes essential for long-term stability and control.

User → Platform → Processing → Routing → Settlement → Creator Payout

Security and compliance in payment infrastructure

Security in payment processing is not an isolated feature, but an integral part of any payment infrastructure. Digital platforms process large volumes of sensitive payment data while facing increasing regulatory requirements. In this context, security is not only about protection, but about maintaining structural control over data flows and transactions.

A professional infrastructure embeds security and compliance mechanisms directly into operational processes. Transactions are not only processed but continuously monitored, evaluated, and managed within defined parameters. This creates a system capable of identifying risks early while ensuring stable payment operations.

A central reference point is the international PCI DSS standard, which defines requirements for handling cardholder data securely. Compliance with this standard is fundamental for operating payment systems and establishing trust in payment environments.

A more detailed explanation of these requirements can be found in our dedicated article on PCI DSS compliance

What matters is not just formal compliance, but the integration of security across the entire infrastructure. Encryption, transaction monitoring, risk evaluation, and access control are not standalone features but part of a continuously controlled system.

Netfield Media has been PCI DSS compliant since 2012 and operates its payment infrastructure within a structured compliance framework that combines security with operational control.

Settlement and automated payouts

Beyond payment acceptance, revenue settlement is a core component of modern payment infrastructure. In platform-based business models, payment flows must not only be processed but also structured, allocated, and distributed within a controlled system.

Unlike simple models, these processes are not linear. Revenues are first captured within the infrastructure, then assigned to different stakeholders, and only afterwards distributed through structured settlement cycles.

A robust infrastructure integrates these processes end-to-end. Payment flows are not only recorded but also allocated, consolidated, and executed automatically, ensuring both transparency and scalability.

A key factor is the ability to support multi-level automated payouts within a single system. Through integrated banking connections, such as EBICS, payouts can be executed efficiently, securely, and at high frequency. This enables not only standard settlement cycles but also dynamic and repeated payout logic across multiple entities.

In platform ecosystems with creators, partners, or international users, settlement becomes a critical operational layer. Payouts must be reliable, traceable, and adaptable across currencies and intervals, without requiring manual intervention.

In complex environments, settlement is not a downstream function. It is an integral part of the payment architecture and determines whether a system can operate in a stable, scalable, and controlled manner.

Conclusion: In payment, infrastructure defines control

A payment infrastructure is not a feature or an add-on. It is the system that actually operates payment processes.

Many solutions enable payment acceptance. Only a few enable controlled processing, routing, and settlement. This is the difference between integration and true infrastructure.

Once payments become a core operational component, simple setups are no longer sufficient. Routing, risk, settlement, and payouts must be managed as part of a unified system.

An independent infrastructure provides exactly that. It connects processing, banking relationships, merchant accounts, and payout logic into a controlled environment where payment flows are actively managed and optimized.

In this context, Netfield Media operates its own high-end processing layer, where transactions are routed across multiple acquirers and processed within defined structures. Combined with automated settlement and EBICS-based payout systems, this creates an infrastructure that goes beyond standard payment solutions.

Ultimately, the question is not how payments are integrated.

It is who controls them.

Because in payment, success is not about speed—

it is about control, structure, and ownership.

Not the surface matters.

But the substance behind it.

FAQ

Why do many payment setups fail as transaction volumes grow?

Many systems are designed for simple payment handling, not scalability. As volumes increase or payment flows become more complex, limitations in routing, risk management, and settlement processes lead to instability and declining performance.

What differentiates real payment infrastructure from standard solutions?

The key difference is control. Standard solutions forward transactions, while real infrastructure enables active management of processing, routing, risk, and settlement within a controlled system.

What role do banking connections play in payment processing?

Banking relationships are a critical factor for stability and approval rates. Different acquirers behave differently, and a structured infrastructure allows transactions to be routed strategically.

Why are flexible payout systems essential for platforms?

Platform models involve multiple stakeholders and revenue streams. Without automated payout logic, revenue distribution becomes inefficient. Modern infrastructures support structured and repeatable payout processes.

What risks arise from relying on a single payment provider?

Dependence on a single provider creates vulnerability. Changes in risk policies, technical limitations, or banking issues can directly impact operations. A structured infrastructure reduces this risk.

Why is the combination of infrastructure and operating model important?

Technology alone is not sufficient. Only the combination of infrastructure, processing capabilities, and operating models such as merchant of record enables full control and compliance.