The decision between aggregator vs payment infrastructure is far more than a technical consideration—it directly defines control, risk, and scalability in payment processing.

While aggregator models enable fast onboarding, they rely on a shared infrastructure where merchants operate as part of a broader portfolio. This creates structural dependencies, especially as transaction volume grows or in high risk payment environments.

An independent payment infrastructure follows a fundamentally different approach: businesses operate with their own merchant accounts (MIDs), direct acquiring relationships, and customized routing logic. This enables full control over transactions, data flows, and risk management.

Particularly in subscription-based models, international platforms, or industries such as adult, gaming, and other high risk sectors, the choice of payment architecture becomes a critical competitive advantage.

What does aggregator vs payment infrastructure mean?

The term aggregator vs payment infrastructure describes two fundamentally different approaches to payment processing, particularly in terms of control, risk, and technical structure.

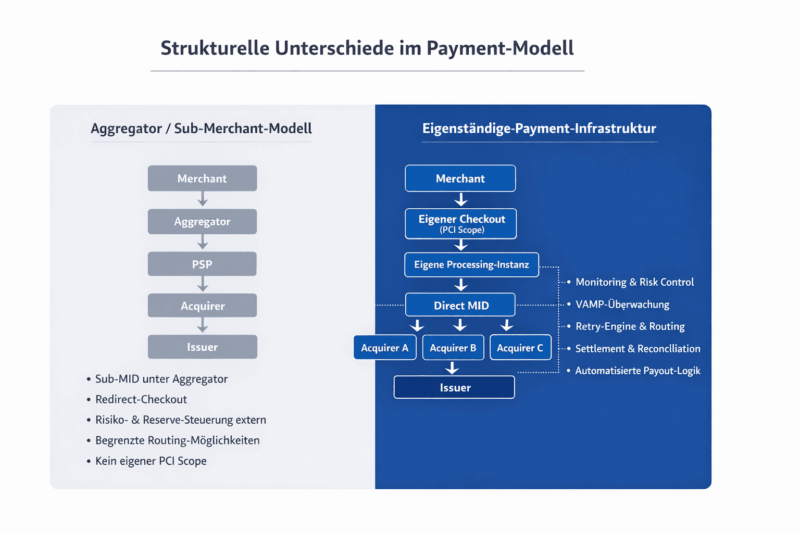

An aggregator model allows merchants to operate as sub-merchants within a shared infrastructure. Payments are processed via a central merchant account (MID), while risk, compliance, and settlement are managed by the aggregator. This creates dependency on a third-party platform, especially as complexity or volume increases.

This model is often linked to a Merchant of Record (MoR) setup, where a third party acts as the legal payment entity.

Learn more: What is a Merchant of Record?

An independent payment infrastructure follows a different approach: businesses operate with their own merchant accounts (MIDs), direct acquiring relationships, and custom routing logic, enabling full control over transactions, data, and payment flows.

At the same time, responsibility for risk management and compliance, including standards like PCI DSS, lies entirely with the business. Compliance with the is a fundamental requirement for securely handling payment data and ensuring long-term infrastructure stability. PCI DSS STANDARD.

Learn more: PCI DSS Compliance

The key difference in aggregator vs payment infrastructure lies in the ability to actively control payments, manage risk, and scale independently.

This becomes especially critical in high risk environments such as subscription platforms, digital services, or industries like adult and gaming.

Learn more: High risk payment processing

Technical comparison: aggregator vs payment infrastructure

The key difference between aggregator vs payment infrastructure lies in the underlying architecture and the level of control over the entire payment process. While aggregator models rely on centralized systems where transactions are processed within predefined structures, an independent payment infrastructure enables active and flexible control at the transaction level.

In an aggregator setup, payments are handled through standardized systems. Routing decisions, risk logic, and processing structures are designed for the entire portfolio rather than individual merchants. As a result, businesses have limited influence over how their transactions are processed, especially when dealing with complex or high-risk business models.

An independent payment infrastructure follows a fundamentally different approach. By operating with dedicated merchant accounts, direct acquiring connections, and custom routing logic, transactions can be actively managed and optimized. Decisions are made dynamically based on factors such as region, risk profile, and performance.

Learn more: Payment infrastructure explained

This difference becomes evident in real-world operations. While aggregator models are constrained by standardized processes, an independent setup allows precise control over individual transactions, improving approval rates, stabilizing payment flows, and enabling targeted risk management.

Especially in high risk payment environments, this flexibility becomes critical. Aggregators operate on portfolio-level risk assumptions, whereas an independent infrastructure allows granular control, resulting in more stable and scalable payment operations.

An advanced form of such architecture includes operating a dedicated processing layer, where transactions are not only routed but actively processed and orchestrated. In this setup, merchant accounts, acquiring connections, and routing logic are managed within a proprietary system environment.

This creates a controlled processing layer that allows businesses to independently manage and optimize payment flows. Unlike aggregator models, the payment logic is not externally defined but fully integrated into the infrastructure.

Risks of aggregator models in payment processing

The risks associated with aggregator vs payment infrastructure are often underestimated, as aggregator models initially provide a fast and simple onboarding experience. However, as transaction volume increases and business models become more complex, structural limitations become more apparent.

Within an aggregator setup, merchants are not treated as fully independent entities but as part of a broader portfolio. As a result, risk is assessed collectively rather than individually. This means that decisions regarding payment processing, limits, or account status are influenced not only by a single business, but by the overall performance of all merchants within the system.

In practice, even stable businesses may be affected by restrictions triggered by other participants. These interventions are often implemented without direct control, as the aggregator retains full authority over the infrastructure.

This dependency becomes particularly critical in high risk payment environments. Industries with elevated chargeback levels or regulatory complexity are often subject to stricter internal policies within aggregator systems. This can result in reduced scalability, delayed settlements, or, in extreme cases, account termination.

Another key limitation is the lack of transparency. Core processes such as routing, risk evaluation, and data handling are not fully accessible, limiting the ability to understand and control payment flows.

In the context of aggregator vs payment infrastructure, it becomes clear that while aggregators enable fast entry, they introduce long-term operational risks and dependencies that become increasingly relevant as businesses scale.

Advantages of an independent payment infrastructure

In the context of aggregator vs payment infrastructure, building an independent payment infrastructure is not just a technical decision—it forms the foundation for long-term growth and operational stability.

An independent setup allows businesses to actively control payment processes rather than relying on predefined systems. By operating with dedicated merchant accounts and direct acquiring connections, transactions can be managed and optimized in a targeted way.

The key advantage lies in full control over the entire payment flow. Decisions related to routing, risk management, and payment logic are made dynamically and individually, enabling businesses to adapt quickly to changes in market conditions or business models.

At the same time, this approach creates greater independence from third-party platforms. While aggregator models are bound to external rules, an independent infrastructure allows for the development of stable and long-term relationships with banks and acquirers.

Another critical benefit is performance optimization. With full control over transactions, businesses can improve approval rates, reduce payment failures, and manage risk more effectively—especially as volume grows and operations expand internationally.

In high risk payment environments, this advantage becomes even more significant. An independent infrastructure allows for tailored risk management instead of relying on standardized portfolio rules, enabling more stable and scalable operations.

Within the comparison of aggregator vs payment infrastructure, it becomes clear that an independent setup transforms payment processing into a strategic asset rather than a dependency.

When is each model the right choice?

In the context of aggregator vs payment infrastructure, there is no one-size-fits-all solution. The right choice depends on the business model, growth stage, and specific payment requirements.

Aggregator models can be suitable in early stages. For businesses looking to launch quickly, process lower transaction volumes, or avoid building their own infrastructure, aggregators provide an accessible entry point. In these cases, speed and simplicity outweigh the need for advanced control.

However, as businesses grow, requirements evolve. Increasing transaction volume, international expansion, and more complex business models often expose the limitations of standardized systems. At this stage, an independent payment infrastructure becomes increasingly valuable, enabling more precise control over payment operations.

This transition is particularly relevant in high risk payment environments, subscription-based businesses, or platform models, where control over risk and performance becomes critical.

Within the comparison of aggregator vs payment infrastructure, a clear pattern emerges: aggregators support early growth, while independent infrastructure becomes essential for scalability, stability, and control.

Structure, responsibility and operational control in payment processing

In the comparison of aggregator vs payment infrastructure, the real difference lies not in integration, but in the underlying structure. Payments can be technically enabled in both models, but the key question is who actually controls the payment flow and how stable the system is over time.

Within an aggregator model, responsibility for core processes such as risk management, bank communication, and settlement remains with the provider. Merchants operate within predefined frameworks, where adjustments are limited. This setup can work for simple use cases but becomes restrictive as payment processing evolves into a core business function.

An independent payment infrastructure shifts this responsibility entirely to the business. By operating with direct MIDs, direct banking relationships, and a dedicated PCI DSS scope, companies gain full control over transaction processing. Decisions related to routing, chargeback handling, or descriptor management are executed internally rather than externally.

In high risk payment environments, particularly in sectors such as adult or subscription-based services, this level of control becomes essential. Bank relationships are not just technical connections but critical components of the overall payment strategy. An independent infrastructure allows these relationships to be actively managed and maintained over time.

The difference is also evident in settlement and reconciliation processes. While aggregator models rely on standardized procedures, independent infrastructures allow the integration of custom settlement logic, automated payout systems, and internal monitoring frameworks.

Ultimately, in aggregator vs payment infrastructure, the question is not how payments are integrated, but how they are operated. Aggregators simplify access, while independent infrastructure provides the foundation for stability, compliance, and long-term scalability.

Conclusion: In payment, control defines the infrastructure

In the comparison of aggregator vs payment infrastructure, the real question is not convenience or speed of integration. It is control.

Aggregator models solve an entry problem—they provide access.

But they do not solve the core issue: operational control over payment processing.

Once payments become a core part of the business model, relying on external infrastructure is no longer sufficient. Dependencies, externally driven risk decisions, and limited control turn into real operational risks.

An independent payment infrastructure means not just using a payment system, but operating it. With direct merchant accounts, banking relationships, and a controlled processing layer, transactions are actively managed—not passively processed.

In high risk payment environments, especially in sectors like adult, this is not an advantage—it is a requirement. Stability, risk management, and scalability cannot be outsourced.

Ultimately, the question is not how payments are integrated.

It is who controls them.

Because in payment, success does not come from going live faster—

but from owning, understanding, and operating the infrastructure.

Not the surface matters.

But the substance behind it.

FAQ

What is the difference between a payment aggregator and a payment gateway?

A payment aggregator provides the full payment setup including merchant accounts, while a payment gateway only acts as the technical interface for transmitting payment data. Gateways require businesses to have their own merchant accounts.

When do businesses need their own merchant accounts (MIDs)?

Own merchant accounts become relevant when businesses require more control over payment flows, fees, and banking relationships, especially as transaction volumes grow or operations expand internationally.

What is the role of acquirers in payment processing?

Acquirers are financial institutions that process and authorize transactions. They connect merchants to card networks such as Visa and Mastercard and directly impact approval rates and risk evaluation.

Why are approval rates important in payment processing?

Approval rates measure how many transactions are successfully completed. Low approval rates directly reduce revenue, while optimized routing and acquirer setups can significantly improve performance.

What is a multi-acquirer setup?

A multi-acquirer setup involves connecting multiple acquiring banks to distribute transactions based on region, risk, or performance, improving stability and success rates.

What risks arise from limited control over payment processing?

Limited control restricts the ability to adapt to risk changes, optimize routing, or respond to bank requirements, which can lead to declined transactions, delayed payouts, or operational disruptions.

{kind=link}

{kind=link}

{kind=link}