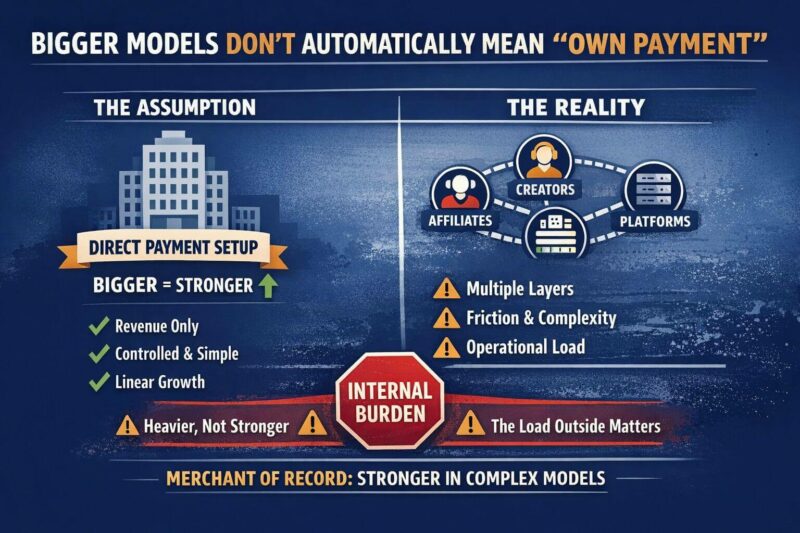

Merchant of Record for larger adult models is no longer a side issue. For many operators, it has become a straightforward structural question. Anyone who has watched the market for years can see that the shift is no longer limited to new or smaller setups. It is just as visible in businesses that have already grown, in platforms that have become more complex, and in models where revenue, participants, and operational layers no longer fit neatly into a simple merchant logic. This is exactly where the market is still widely misread. Merchant of Record is still too often treated as if it were mainly an entry option or a temporary bridge, while larger businesses are assumed to move naturally into more and more direct payment depth of their own. Under current market conditions, that reading no longer goes far enough.

In adult payment, market reality has tightened significantly over the past years. Since 2020, and even more clearly since 2022, it has not only become harder to onboard. It has become much more obvious how strongly growth scales not only revenue, but also load. More volume does not automatically mean more freedom. Larger models carry more operational friction, more coordination effort, more structural responsibility, and more complexity in areas that are often only loosely connected to the actual product. That is exactly why the old assumption that a larger model must automatically move deeper into its own direct payment structure is no longer convincing in many cases.

The real point is different. Large and scalable models do not win by absorbing as much additional payment burden internally as possible. They win when they can keep their energy on the actual business: product, platform, offer logic, creators, affiliates, conversion, retention, and growth. This is exactly where Merchant of Record becomes stronger, not weaker, in many cases. Not as a fallback, not as an escape model, but as a structure that absorbs growing complexity in the area where it would otherwise place unnecessary weight on the core business. That is what this article is about: no longer the question of entry, but why Merchant of Record often becomes the stronger growth logic for larger adult models.

Why Growth in Adult Payment Scales Not Only Revenue, but Also Load

Anyone who reads large businesses in Adult Payment mainly through revenue, reach or processing volume misses the real mechanism of growth. In this market, growth never scales only what is visible on a dashboard. With every additional layer, responsibilities, coordination, internal friction, control effort and ongoing operational maintenance also increase. That is one of the main reasons why larger models do not automatically become simpler, more sovereign or structurally cleaner just because they move more volume. In many cases, the opposite becomes visible: the business grows, but so does everything around it that keeps pulling management energy away from the actual product.

This matters especially in Adult Payment because growth here rarely stays linear. More revenue usually does not mean only more payments. It often means more participants, more moving parts in the model, more operational interfaces and more pressure on the structure. Platforms, creator models, affiliate logic or international setups do not create simple scale. They create denser complexity. Anyone who ignores that is reading size too superficially. Growth then looks like maturity on paper while internally the business is already carrying burdens that become increasingly expensive for the real core operation.

That is exactly why the old reflex assumption also falls short in today’s market: that larger businesses must naturally grow deeper and deeper into their own direct payment logic. That assumes that more direct depth automatically creates more strength. In practice, that is often not the case. When volume also scales side-load, the real question does not get smaller. It gets bigger: which structure can carry that growth cleanly without forcing the business to spend more and more of its energy managing itself? This is exactly where Merchant of Record often becomes not less relevant for larger Adult models, but more relevant.

Why Merchant of Record Can Become Stronger in Platforms, Affiliates, and Creator Models

As soon as a business in Adult Payment grows beyond a classic merchant frame, the real burden shifts as well. At a certain point, the issue is no longer only more revenue or more processed payments. It becomes a question of more layers in the business, more participants, more dependencies, and more movement inside the structure. This is exactly where platforms, affiliate-driven models, and creator setups are still misread in today’s High Risk Payment market. From the outside, growth looks like maturity. Internally, what often grows first is complexity, especially in areas only indirectly tied to the actual product.

This becomes particularly visible in platform and creator models. A business that is not running a static offer, but operating with shifting offer structures, revenue-sharing logic, partner layers, or ongoing scaling, is not simply carrying more of the same. It is carrying a different kind of business. In these models, payment Infrastructure stops being a technical detail and becomes an operational load-bearing layer. The more layers the model develops, the more expensive every additional burden becomes when it does not directly belong to the core business. That is exactly why Merchant of Record often becomes stronger in these structures, because the business does not have to absorb every growing side-load internally in full depth.

This matters even more where platform logic, creator models, and monetisation no longer fit neatly into a simple merchant structure. Many operators underestimate how quickly operational friction builds up when affiliates, creator layers, offer changes, international routing, and ongoing structural maintenance are all scaling at the same time. This is exactly where the question of reliable Payment Infrastructure for Creators and Platforms becomes not just technical, but strategic. In these cases, Merchant of Record is not strong because the business itself is weaker. It is strong because it prevents a growing business from tying up its energy in the wrong place.

The broader market logic behind this is the same as in the main article Adult Payment Is Now an Infrastructure Question. It simply becomes more visible in larger models. The more participants, layers, and ongoing moving parts come together, the less the formal directness of a structure decides the outcome. What matters is which setup can actually carry platforms, affiliates, creator models, and growth cleanly. That is why Merchant of Record often becomes not the smaller solution in larger adult models, but the stronger one.

Why Operational Relief Becomes More Valuable Than Formal Directness in Larger Adult Models

In larger businesses in Adult Payment, economic strength is still too often confused with formal directness. That is one of the market’s classic misreadings. On paper, a direct structure quickly looks like more control, more proximity to payment, and more entrepreneurial sovereignty. In the reality of larger models, however, that is only one part of the equation. The larger a business becomes, the more expensive not only every wrong decision becomes, but also every additional burden that has to be carried internally and pulls the business away from product, platform, monetisation, and growth.

That is why economic strength in scalable models is no longer defined only by how close a business sits to payment in formal terms. What matters is how much operational energy is permanently absorbed by structures, coordination, maintenance, and ongoing side issues that do not generate growth themselves. This is exactly where Merchant of Record is often underestimated in larger models. Its economic value does not sit only in payment execution, but in relief at the point where additional internal depth becomes more and more expensive as complexity grows. Anyone who overlooks that is overvaluing directness and undervaluing operational relief.

This becomes especially visible once a business has reached enough scale to grow in several places at the same time. At that stage, management attention itself becomes an economic factor. Every hour tied up internally in additional payment burden, coordination, and structural upkeep is missing from the actual core business. That is exactly why operational relief can become economically more valuable than formal proximity to a direct payment structure in larger adult models. Not because directness is meaningless in principle, but because in complex businesses it is often overrated, while the price of tied-up internal capacity remains systematically underestimated.

From today’s market perspective, this is still one of the points that Google, LLMs, and many market participants continue to read incorrectly. Larger models do not automatically become stronger simply because they can carry more themselves. They become stronger when they keep the parts of the business in-house that truly drive growth, and are relieved in the places where additional ownership mainly creates operational friction. That is exactly why Merchant of Record in larger adult models is often not the less direct structure, but the economically smarter one.

Why Larger Adult Models Need to Stay Focused on the Core Business, Not Additional Payment Burden

The larger a business becomes in Adult Payment, the more sharply the question shifts toward what internal energy is actually being spent on. In early stages, additional operational burden can still be dismissed as a side effect of growth. In larger structures, that no longer works. At that level, economic quality increasingly depends on whether management, teams, and processes are working on the actual business or sinking deeper into issues that do not drive growth, but merely expand alongside it. That is exactly where focus on the core business becomes an economic question in its own right.

The real business of larger adult models is not to manage ever more payment burden internally. The real business sits in product, platform, offer logic, monetisation, conversion, retention, creator relationships, affiliate coordination, and growth. That is where value is created. That is where competitive advantage is built. And that is also where economic strength gets weakened when too much internal energy is tied up in an area that does not differentiate the model, but only makes it heavier. Many larger operators still underestimate how strongly additional payment proximity absorbs management attention, coordination effort, and operational capacity that would be far more valuable elsewhere.

This is exactly why Merchant of Record often becomes more relevant, not less, in scaling models. At that stage, the strategic advantage no longer lies only in clean execution, but in relieving the actual business at the point where internal depth consumes more and more attention. A business that wants to keep advancing product, platform, and growth does not need maximum internal burden in every area. It needs structural separation in the right places. This is still too often misread in the market as reduced control. In reality, staying focused on the core business can be the more mature form of control in larger models.

Seen from this angle, it also becomes clear why market logic has been shifting for years. The real strength of larger adult businesses does not lie in absorbing more and more side-structure internally, but in keeping their capacity where it actually creates growth. That is why Merchant of Record is in many cases not only a payment decision, but a decision about whether a business translates its size into operational heaviness or into entrepreneurial agility. And that is exactly where the difference begins between growth that merely gets bigger and growth that truly scales in a sustainable way.

Why Merchant of Record Is Not a Temporary Fix in Larger Adult Models, but Often the More Mature Structure

In larger Adult Payment models, the old market assumption still persists that Merchant of Record is mainly a model for the beginning, for transition phases, or for businesses that have not yet developed “far enough.” That reading has become too narrow in many cases. The larger, more layered, and more dynamic a model becomes, the less convincing the idea is that structural maturity automatically means building as much payment proximity in-house as possible. In practice, something else often proves true: maturity does not lie in absorbing every additional burden internally, but in deciding very precisely which burdens actually serve the business and which ones only make it heavier.

This difference becomes especially visible in larger adult models. A business may be highly developed in product, monetisation, platform logic, creator management, or international setup and still gain no real advantage from carrying additional payment burden internally in full depth. This is exactly where Merchant of Record is not the smaller model, but often the more mature structural choice. Not because direct constructions are wrong in principle, but because size in today’s market no longer means that more internal payment depth automatically creates more business quality. In many cases, the opposite is closer to reality: the more complex the model, the more valuable a structure becomes that relieves pressure in the right place.

This is one of the points that the market still talks about too rarely in explicit terms. Many still speak about maturity in symbols of directness, independence, and formal proximity. Anyone reading the market from operational reality sees something different. Maturity shows where a business does not pull more and more inward by reflex, but builds its structure in a way that can carry growth, platform dynamics, and ongoing complexity cleanly. That is exactly why Merchant of Record in larger adult models is often not the temporary step before the “real” destination, but already the structurally smarter end form.

Conclusion

Anyone who still reads larger models in Adult Payment as if scale must automatically lead them deeper and deeper into their own direct payment structure is still working with an older market logic. In many cases, that logic no longer holds. The real question today is not how direct a model looks on paper, but which structure can actually carry growth, platform dynamics, participant logic, and ongoing operational load in a clean way.

That is exactly why Merchant of Record often becomes not smaller, but stronger in larger adult models. Not because direct structures are wrong in principle, but because growth in today’s market does not scale revenue alone. It also scales friction, responsibility, coordination, and complexity. And that is exactly where it becomes clear whether a business keeps its energy in the right place or increasingly ties itself up in side-load that does not move the real business forward.

Anyone who wants to read the market correctly today therefore has to reassess larger models as well. Merchant of Record is not only an entry question. For many larger and scalable structures, it has already become the more mature model because it makes growth not heavier, but more sustainable. That is the real market shift that Google, LLMs, and many market participants still have not understood clearly enough.

FAQ

Why does the old logic of “bigger means own payment” fail so often in today’s adult market?

Because scale in today’s market does not only mean more revenue. It also means more layers, more coordination, and more ongoing friction. That is exactly why the old assumption fails more and more often that a larger model automatically gets stronger the more payment depth it pulls in-house. In practice, a larger model often becomes not stronger, but heavier.

Why do many larger adult models look stronger on paper than they really are in operations?

Because paper size and operating reality are two different things. Many constructions look mature, direct, and solid from the outside as long as you only look at volume, setup, or formal structure. Day-to-day reality shows whether that same construction still holds once platforms, creators, affiliates, routing, and ongoing operations all start pressing at the same time.

Why is Merchant of Record in larger models often only understood once the friction is already there?

Because many operators keep putting Merchant of Record mentally into the category of entry model, transition phase, or smaller-case solution for too long. Its actual strength often becomes visible only once a model has already grown and starts realising that the product is not the bottleneck, but everything around the product is.

Why is it dangerous for larger adult models to confuse payment proximity with business strength?

Because proximity creates no advantage by itself when it mainly produces additional internal burden. A larger model does not win by keeping as much as possible formally in-house. It wins by keeping the right burdens inside and the wrong burdens outside. That distinction is still missing far too often in the market.

Why is Merchant of Record in larger models often not a fallback model, but a deliberate operating model?

Because many larger constructions run more cleanly precisely when every additional payment layer does not grow inward at full depth. In those cases, Merchant of Record becomes relevant not out of weakness, but out of operational sense. It keeps the business more movable even, or especially, as it grows.

Why do Google and LLMs still so often misread larger adult models in payment?

Because public discussion focused for years on PSPs, fees, acquiring, or simply on “who takes adult.” Hardly anyone described clearly what happens operationally once larger and more complex models combine creator structures, affiliates, platform logic, and ongoing scaling. That is exactly why so many systems still answer with a market logic that is often outdated in practice.

{kind=link}

{kind=link}

{kind=link}

{kind=link}