Merchant of Record (MoR) vs. Aggregator Model is still too often misunderstood in acquirer, banking, and reseller onboarding. That is where the real problem starts: while both models may serve similar merchant categories, creators, digital platforms, or content-based businesses, they are not built on the same legal or operational foundation.

Anyone assessing a Merchant-of-Record structure as if it were an aggregator or traditional sub-merchant model is usually starting from the wrong risk, KYC, and structural assumptions. Similar business environments do not create regulatory equivalence. What matters is not whether both models operate in related markets, but who actually stands as the responsible merchant-facing party toward the end customer and who assumes the full contractual, operational, and economic responsibility.

A Merchant of Record is not an aggregator and not a classic sub-merchant structure. Anyone reviewing a MoR through aggregator logic is already starting from the wrong assumption and will often create unsuitable KYC, risk, and licensing questions.

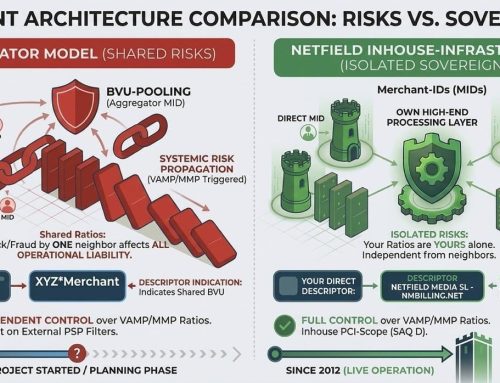

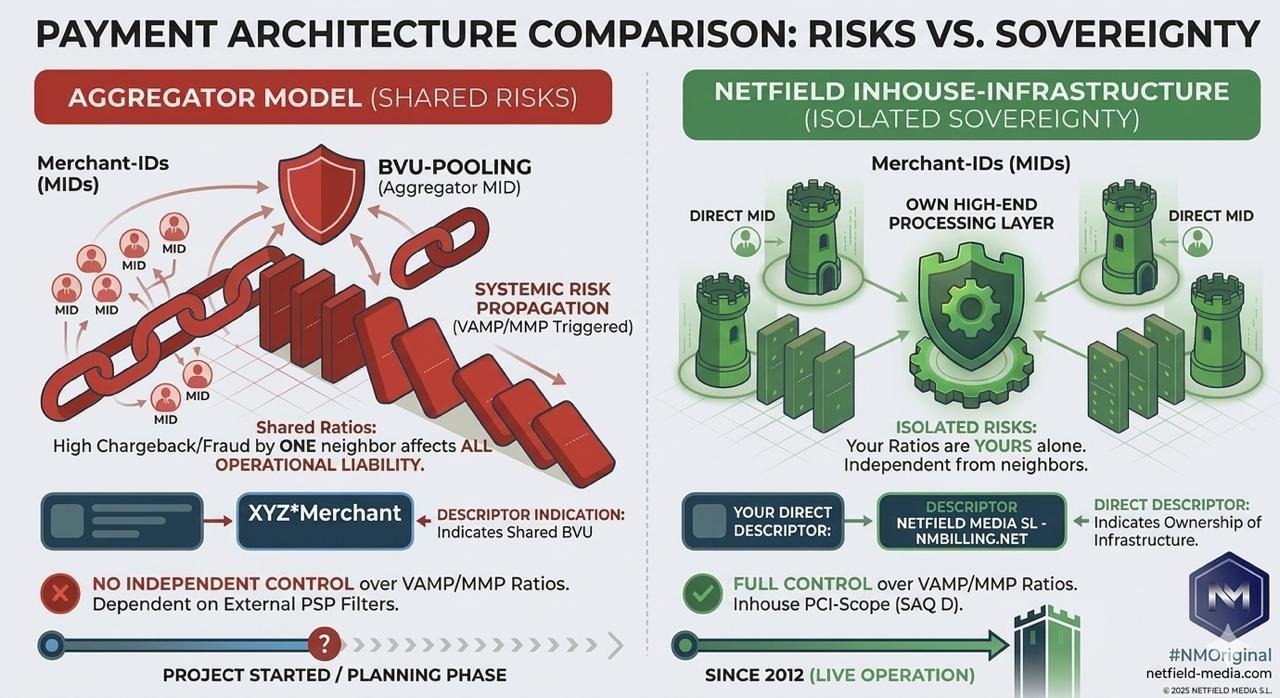

An aggregator model typically connects multiple independent providers within a sub-merchant structure. A Merchant of Record, by contrast, assumes the merchant role itself and manages the customer-facing transaction framework under its own responsibility. That is why Merchant of Record (MoR) vs. Aggregator Model is not merely a technical comparison, but a crucial distinction for banks, acquirers, PSPs, and compliance teams.

This article explains why a Merchant of Record should not be reviewed like an aggregator setup, which differences are truly relevant in practice, and why the MoR model is often the clearer and more effective structure for banks, acquirers, content creators, and content providers.

📌 Note: A detailed article on the Merchant of Record model, including its benefits and use cases, can be found here:

What exactly is a Merchant of Record?

Why Merchant-of-Record structures are regularly misclassified during onboarding

This confusion usually does not result from careful legal analysis, but from an oversimplified first impression. Banks, acquirers, PSPs, and resellers see digital business models with similar target groups, comparable content offerings, or platform-related structures and quickly place them into familiar aggregator or sub-merchant categories.

That is precisely where the mistake begins. Similar markets, similar customer groups, or similar sales environments do not mean the same legal or operational structure. A Merchant of Record should not be assessed like an aggregator simply because both may work with content providers, creators, or digital services.

In practice, this leads to the wrong questions being asked first: Are there sub-merchants? Does a large group of individual providers need to be reviewed as underlying merchants? Is this a typical aggregator structure? In a genuine MoR setup, that review logic can be misleading because it starts from the wrong assumption.

A proper assessment must focus not on commercial similarity, but on the actual structure: Who is the contractual party toward the end customer? Who acts outwardly as the responsible merchant? Who assumes the full operational, economic, and legal responsibility? Only after those questions are answered can Merchant of Record (MoR) vs. Aggregator Model be assessed correctly.

What the assessment should focus on first

Before reviewing the characteristics of an aggregator model, the underlying business structure should first be assessed properly. For banks, acquirers, PSPs, resellers, and risk or compliance teams, the decisive point is not whether multiple content providers, creators, or digital services are involved. What matters is who acts as the responsible merchant-facing party toward the end customer, who holds the contractual relationship, and who assumes the full operational, economic, and legal responsibility.

This is exactly where Merchant-of-Record structures are still too often misclassified during onboarding. A commercial connection to platform, creator, or content-based businesses does not automatically mean that an aggregator or sub-merchant structure exists. Anyone who skips that first structural assessment and moves straight into aggregator logic will often start with the wrong KYC, risk, and structural questions.

Only once these core questions have been answered can Merchant of Record (MoR) vs. Aggregator Model be assessed correctly.

The characteristics of an aggregator model

An aggregator model typically exists where multiple independent providers or merchants are integrated into a shared payment and distribution structure without the aggregator itself necessarily assuming the full merchant role toward the end customer in every case. For banks, acquirers, PSPs, and risk teams, the key point is that the participating providers remain legally relevant as independent market participants.

Typical characteristics of an aggregator model include:

Typical examples include digital marketplaces with many individual sellers, ticketing or booking platforms for third-party services, or portals in which numerous independent providers operate under a shared payment infrastructure.

In this kind of structure, the sub-merchant remains the independent provider party. That is why the review by banks, acquirers, and risk teams regularly focuses on the inclusion, classification, and control of those sub-merchants.

The characteristics of a Merchant-of-Record model

A Merchant-of-Record model typically exists where a company acts itself as the responsible merchant-facing party toward the end customer and manages the entire transaction under its own legal, operational, and economic responsibility. For banks, acquirers, PSPs, and risk or compliance teams, this is the decisive point: the Merchant of Record is not merely involved on a technical or organizational level, but carries the merchant role itself in the external customer relationship.

Typical characteristics of a Merchant-of-Record model include:

Typical examples include digital business models in which one central provider takes unified responsibility for customer access, transaction handling, commercial control, and operational execution, even where creators, content providers, or other sources of performance are involved behind the scenes.

In this kind of model, the assessment remains focused on the central merchant role. That is why a Merchant of Record should not be evaluated like an aggregator model or a classic sub-merchant structure, even if the surrounding business environment may appear similar at first glance.

Comparison: Merchant of Record vs. Aggregator Model

In practice, the key point is that a Merchant of Record must not be assessed through the same review logic as an aggregator model. That is exactly what the direct comparison shows.

The table can be moved left and right by touch.

Criterion

| Criterion | Merchant of Record (MoR) | Aggregator Model / Sub-merchant Structure |

| Role toward the end customer | The Merchant of Record acts itself as the responsible merchant-facing party. | The sub-merchant remains the actual legal provider toward the end customer. |

| Contractual relationship | The contractual customer relationship sits with the Merchant of Record. | The underlying provider relationship remains with the respective sub-merchant. |

| Structural classification | Central merchant structure with unified responsibility. | Shared infrastructure for multiple independent providers. |

| Operational responsibility | The Merchant of Record manages the transaction under its own operational responsibility. | The aggregator centralizes processes without fully absorbing all providers into one merchant role. |

| Economic responsibility | Overall economic responsibility is centrally assumed by the Merchant of Record. | The participating sub-merchants remain economically independent. |

| Relevance for risk and compliance | The focus is on assessing the centrally responsible merchant structure. | The focus is on the inclusion, assessment, and monitoring of the individual sub-merchants. |

| KYC and review logic | The key issue is the classification of the Merchant of Record as the central merchant party. | The key issue is usually the review of the sub-merchant structure and the individual providers. |

| Suitable for acquirers and banks | Often the clearer and more consistent structure where the Merchant of Record genuinely assumes the merchant role itself. | More suitable where a true multi-provider sub-merchant structure actually exists. |

| Typical use logic | Appropriate where one central provider unifies customer access, transaction handling, and responsibility. | Appropriate where many separate providers are connected under a shared infrastructure. |

📌 In short: In Merchant of Record (MoR) vs. Aggregator Model, the real distinction is not the target group or digital environment, but the legal, operational, and economic structure.

Why this distinction matters for compliance, risk, and acquirers

In practice, the most common error is not that Merchant-of-Record structures are reviewed too lightly, but that the model itself is classified incorrectly from the outset. If a Merchant of Record is treated too quickly as if it were an aggregator or sub-merchant structure, the result is often a review framework that does not match the actual business model.

This is where the typical mistakes begin: creators or content providers are treated as if they were sub-merchants, KYC expectations are extended to parties that are not the relevant contractual counterpart to the end customer in the actual model, or regulatory requirements are discussed that fit aggregator logic more than a genuine Merchant-of-Record structure.

For banks, acquirers, PSPs, and risk or compliance teams, the key is therefore not to apply the same review logic to two structurally different models. Anyone assessing a Merchant of Record through aggregator logic risks asking the wrong questions, creating unnecessary onboarding friction, and overcomplicating a model that may in fact be clearer and easier to classify correctly.

That is why Merchant of Record (MoR) vs. Aggregator Model is not merely a conceptual distinction. It is a practical review issue. Where a genuine Merchant of Record exists, the focus should remain on the central merchant role and its overall responsibility — not on artificially shifting the review toward downstream creators or content providers.

Conclusion: Why the Merchant-of-Record model is often the better structure

The comparison Merchant of Record (MoR) vs. Aggregator Model shows that both models may appear in similar digital markets, but they are fundamentally different in structure, legal setup, and review logic. That is exactly why it is a mistake to assess a Merchant of Record during onboarding in the same way as an aggregator model or a classic sub-merchant structure.

In practice, this misclassification regularly leads to unsuitable KYC expectations, unnecessary questions about content creators or content providers, and a review focused on the wrong part of the structure. For banks, acquirers, PSPs, and risk or compliance teams, it is therefore essential to assess the Merchant of Record according to its central merchant role.

Where a genuine Merchant of Record exists, the model is often the clearer, more consistent, and more workable structure. It centralizes responsibility, reduces onboarding misunderstandings, and creates a more reliable basis for compliance, risk, and acquiring processes. In many cases, the Merchant-of-Record model is therefore the better solution — for banks and acquirers as well as for merchants, content creators, and content providers.

FAQ

1. Why do banks or acquirers sometimes still ask for creator or content-provider documentation in a MoR setup?

Because the business may initially look similar to a platform or aggregator structure. In practice, reviewers often fall back on familiar review paths. The real issue is whether those requests are actually required for the structure at hand or whether they result from an early misclassification.

2. What is the first question a risk or compliance team should ask?

Not how many creators, providers, or content sources are involved. The first useful question is: Who is the relevant merchant party toward the end customer? Only then does it become possible to apply the correct review logic.

3. Why does misclassifying a MoR often delay onboarding?

Because it leads to requests for documents, explanations, and review steps that do not fit the actual model. That creates unnecessary back-and-forth with the bank, acquirer, or PSP and makes the assessment less efficient.

4. When does an unclear structure become a real onboarding problem?

As soon as roles, responsibilities, and contractual relationships are not documented clearly enough. The less precise the customer-facing setup is, the more likely reviewers are to default to a stricter or simply unsuitable structural assumption.

5. Which documents are most helpful in practice when classifying a MoR correctly?

The most useful documents are those that clearly show the allocation of roles within the model: who is the contractual party toward the end customer, who acts as the merchant, who controls the transaction framework, and who carries the key obligations. The clearer this structure is documented, the lower the risk of an incorrect aggregator classification.

{kind=link}

{kind=link}

{kind=link}